A Market Signals subscriber from beautiful Brazil inquired about the possibility of using a leveraged ETF in place of SPY ETF, or even account margin, for boosting the performance of our MRSPYW weekly mean-reversion strategy. Below is our analysis.

MRSPYW is one of six strategies that generate signals in the weekly timeframe for our Market Signals subscription service. The strategy trades long-only SPY in mean-reversion mode. The strategy is not data-mined but based on a formula from a text on probability theory that models price action dynamics. Trades are entered and exited at the open of the first trading day of the week. The strategy incorporates bear market downside protection but it does not implement stop-loss, as this is common with mean-reversion.

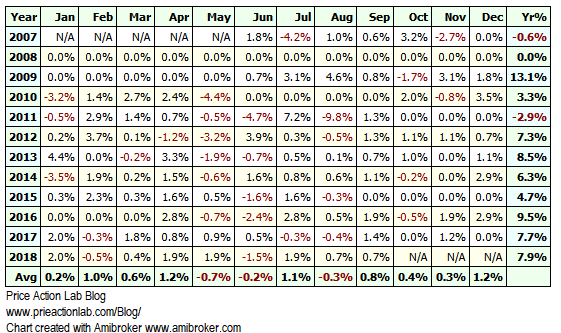

Year-to-date the strategy is gaining 7.9% at 5.7% maximum drawdown based on backtests with $0.01/share commission included.

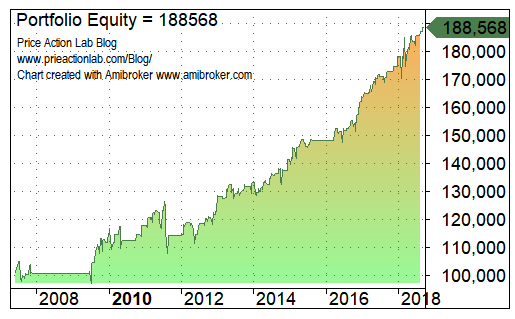

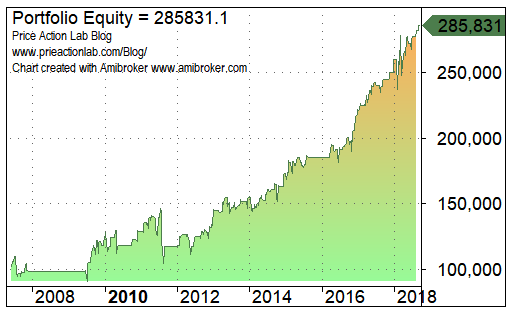

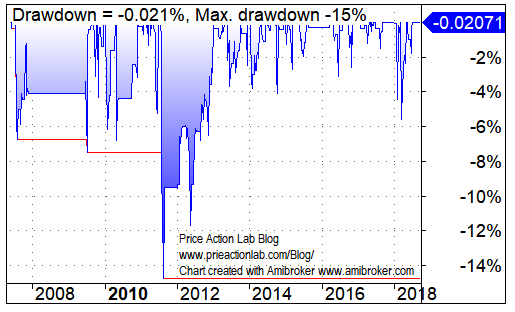

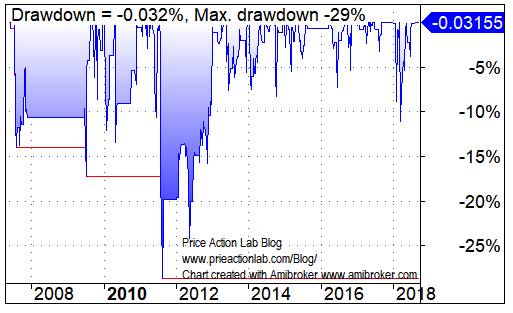

The performance of this strategy can be leveraged either by increasing the allocation in a portfolio, by employing a leveraged ETF, or by using account margin. For example, SSO offers 2x the performance of SPY. Below we compare the performance of two strategies: one based on SPY ETF and another based on signals for SPY ETF that are used to trade SSO instead. Backtests start in June 2007 and end 09/28/2018. Commission is $0.01/share and equity is fully invested. All entries and exits are for the open of the week. Click on images to enlarge.

Equity curves

SPY ETF |

SSO ETF |

Drawdown profile

SPY ETF |

SSO ETF |

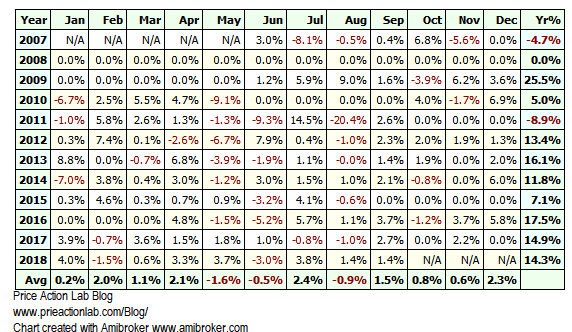

Monthly returns

SPY ETF |

SSO ETF |

Performance summary table

| Parameter | SPY ETF | SSO ETF |

| CAGR | 5.8% | 9.7% |

| Max. DD | -14.8% | -28.7% |

| Sharpe | 0.89 | 0.69 |

| MAR | 0.56 | 0.45 |

| Trades | 113 | 113 |

| Win rate | 71.7% | 69% |

| B&H CAGR | 8.0% | 9.9% |

| 50% margin CAGR | 11.3% | – |

Using margin

If 50% margin account is used that doubles purchasing power, CAGR for the SPY strategy is 11.3% at 29.2% drawdown in the same period. Specifically, the difference is about 160 basis points in favor of a margin account. CAGR is higher with 50% margin as compared to using SSO due to “volatility drag” that affects leveraged ETFs. This effect can be seen from the above performance summary table: buy and hold CAGR for SPY is 8% but for SSO it is not doubled but only about 10% due to volatility drag induced, especially from the 2008 market crash. Note that since 06/01/2010, CAGR for SPY is 15% versus 27.5% for SSO as volatility drag has been reduced. These numbers may also account for different management fees.

There are additional issues with trading leveraged ETFs and/or a margin account. Check with your broker about maintenance margin for leverage ETFs and for trading ETFs on margin in general.

Summary

Using 50% margin appears to offer higher returns in backtests but other considerations must be also taken into account, such as interest charged on borrowed funds and maintenance margin requirements. After all factors are taken into account, there is probably little difference between short-term trading based on 2x leveraged ETFs and trading on a margin account. However, large deviations can result due to specific broker requirements in addition to exchange regulations. The most important result from this article is that any attempt to increase returns comes with a proportional increase in maximum drawdown and there is no way around this unless complicated synthetic products are used, something that is beyond the scope of this article and blog.

If you found this article interesting, I invite you follow this blog via any of the methods below.

Subscribe via RSS or Email, or follow us on Twitter

If you have any questions or comments, happy to connect on Twitter: @mikeharrisNY

Charting and backtesting program: Amibroker

Market signals from systematic strategies are offered in our premium Market Signals service. Stock signals are offered daily in our Premium Stocks report. For all subscription options click here.