Long-only 12-month price series momentum in S&P 500 total return registered a loss of 7.5% in 2018 versus a gain of 1.2% for the 50/200 cross in daily timeframe. Below are the details.

We consider the following two strategies:

Monthly timeframe

Buy at next open when price crosses above the 12-month moving average.

Sell at next open when price crosses below the 12-month moving average

Daily timeframe

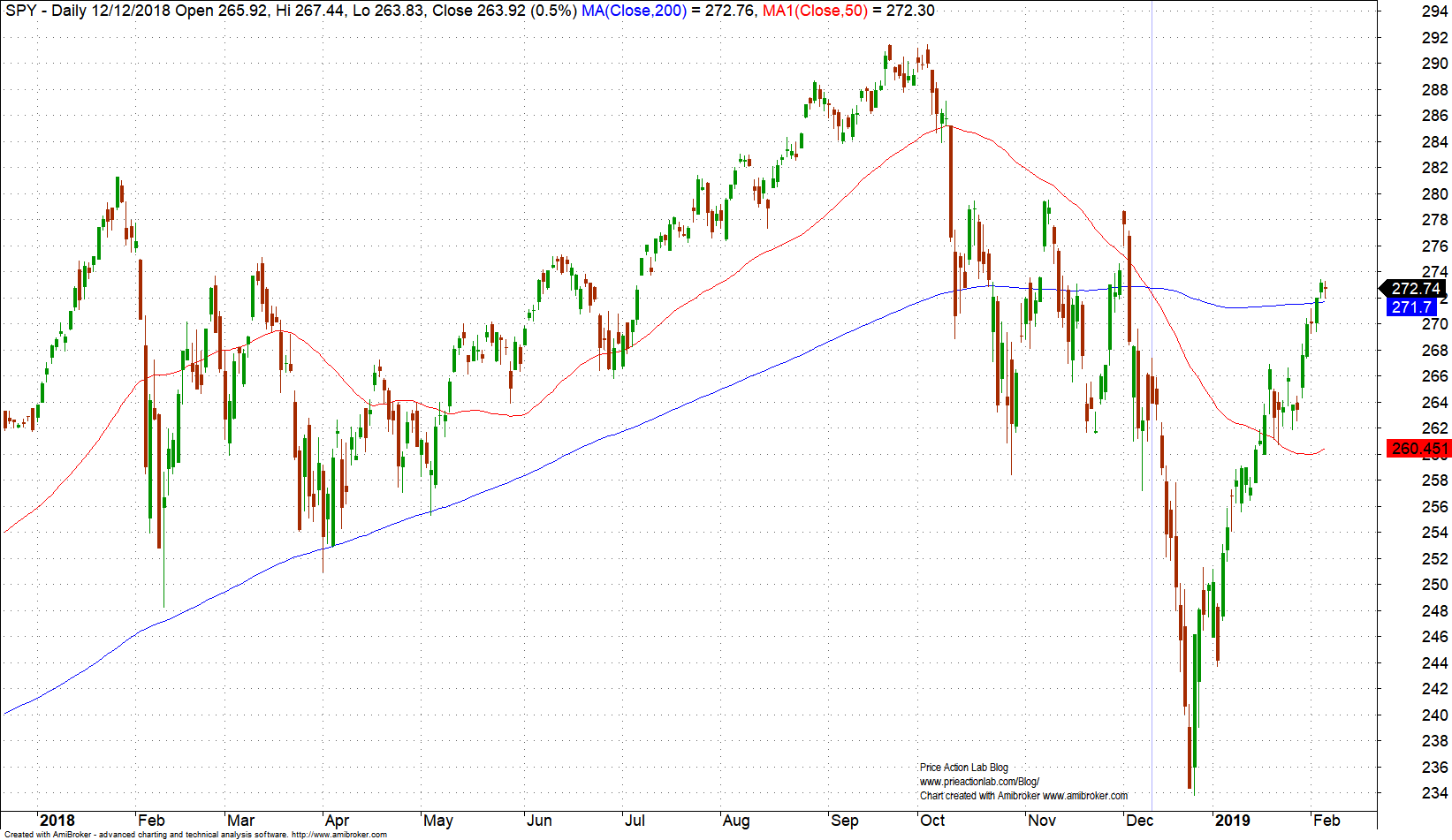

Buy at next open when 50-day moving average crosses above the 200-day moving average

Sell at next open when 50-day moving average crosses below the 200-day moving average

Below are backtest results for SPY ETF from 01/02/2008 to 02/06/2019 with $0.01 commission per share included. Click on images to enlarge.

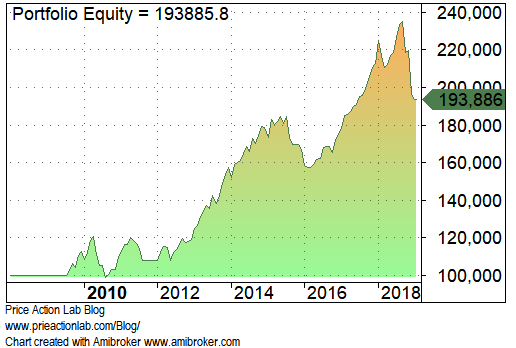

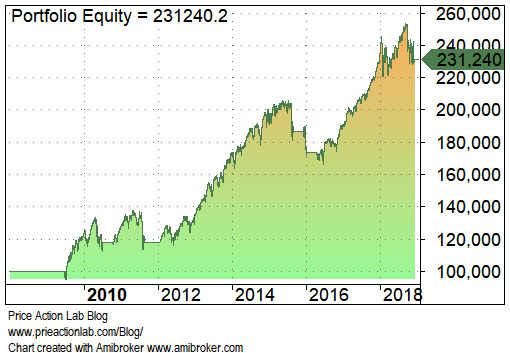

Equity curves

1M12 cross |

50/200 cross |

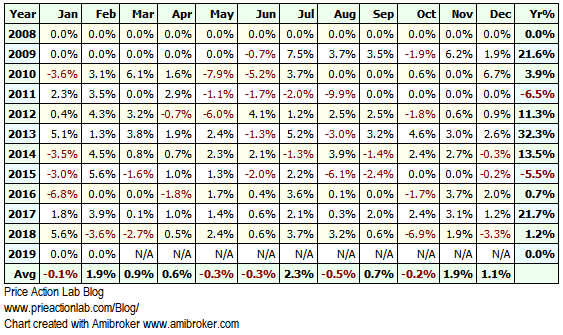

Monthly returns

1M12 cross |

50/200 cross |

The monthly strategy lost 7.5% in 2018 while the daily strategy gained 1.2%. This is what happened:

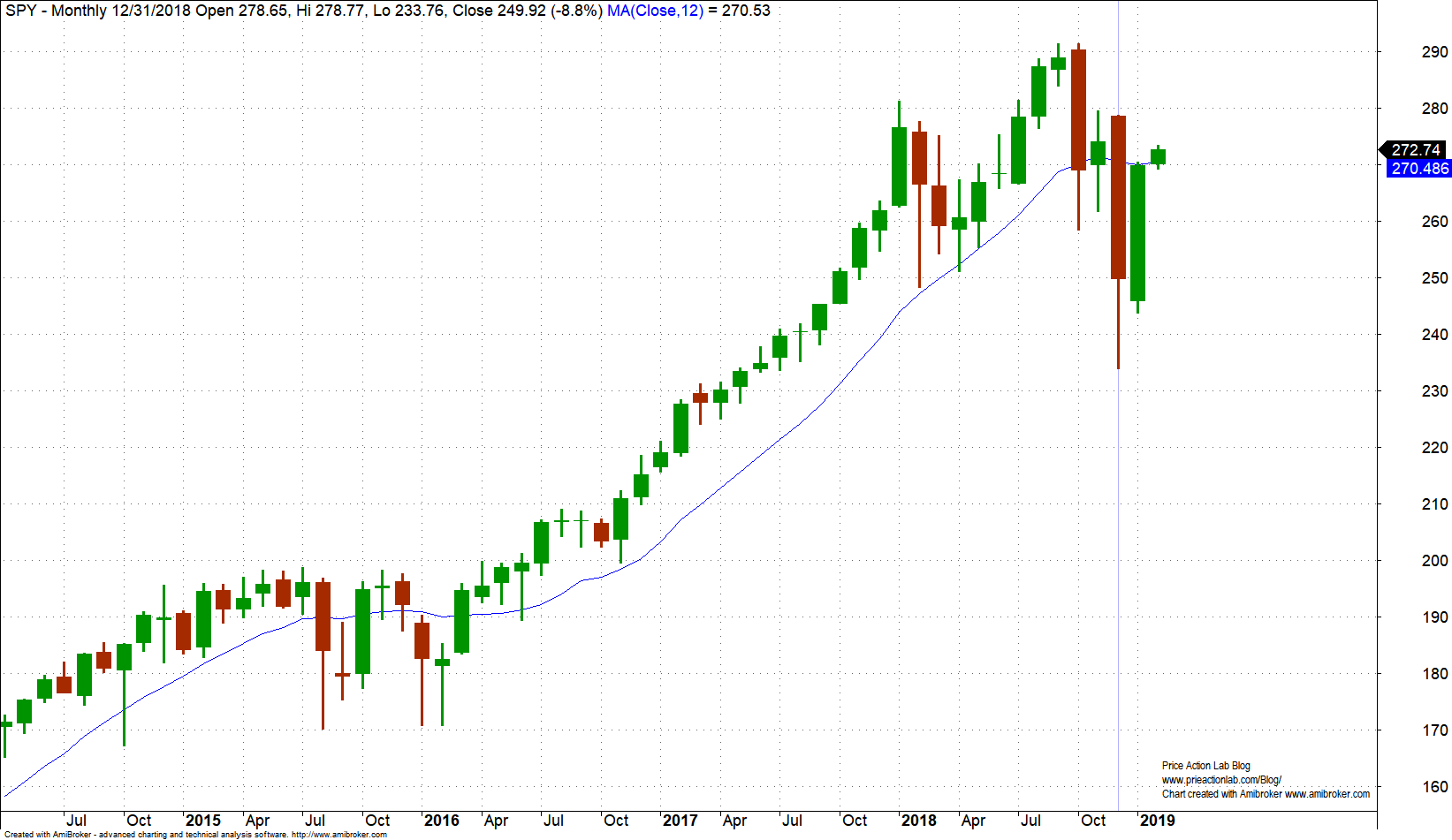

The monthly strategy was not fast enough in exiting the market as shown in the above chart and on top of that the open of the next month was lower. On the other hand, the daily strategy avoided most of the drawdown, as shown below:

Now, some may claim that they wait one month before exiting. Well, in case the correction was not over they would have faced even higher losses.

In fact, you cannot know in advance if a delay is appropriate and it may be a better practice to get out as soon as a faster signal is received.

Sometimes is better to use the daily timeframe, during other times it may be not. It is all random and depends on the particular path the market takes. In this particular case faster action made a big difference.

If you found this article interesting, I invite you follow this blog via any of these methods below:

RSS or Email, or follow us on Twitter

If you have any questions or comments, happy to connect on Twitter: @mikeharrisNY

Market signals from systematic strategies are offered in our premium Market Signals service. For all subscription options click here.