Some random traders will always outperform the market. Financial media often submits to sensationalism and fails to convey the essential message.

About a week ago, Dave Portnoy stunned financial social media by describing to a fund manager how to pick stocks using scrabble letters. Some of us who were trading the markets before the dot com crash remember the studies with monkeys throwing darts on walls covered with newspaper quotes and outperforming portfolio managers.

Dave Portnoy’s point , as well as of those academics with the random monkey stock picks 20 years ago, was to show that in strong bull markets it is hard to pick stocks and you may have better odds choosing them at random. Timing strategies have the risk of generating worse than random returns but this is something beyond the scope of this brief article. Most people cannot manage the complexity required to beat the market and are better off buying and holding. Therefore, I believe Dave Portnoy’s message was that if you cannot outsmart the market, just follow a few leaders and hope that luck will be on your side.

I cannot emphasize enough how important is Dave Portnoy’s message for most traders and investors that have no edge. I have written many articles about random trading but I still think many do not get it, especially the financial media gets it wrong in many cases: Random trading will not get you ahead in most cases. But when random trading outperforms during bull markets, maybe buying and holding is the optimum strategy.

Given a large population of random traders, some will outperform the market because of luck in choosing a security or portfolio of securities that beat the benchmark. However, some other random traders will underperform the market. The performance of the ensemble of all traders will in most cases be close to market performance in short periods of time and depending on some known and unknown factors. Let us look at an example below.

Let us assume that on March 23, 2020, someone knew the market bottom was in place and purchased 10 stocks at random from NASDAQ-100. The performance from March 23, 2020 to June 23, 2020, of this random portfolio represents only one possible path in the time domain. In fact, for 10 stocks in a portfolio from 100 possible alternatives, there are trillions of possible portfolios, or trillions of possible paths in the time domain.

Below is the equity curve of a random path. The 10 random stocks are also shown on the chart with the trade details. Commission of $0.01/share is included.

The random portfolio return was 54.6% and that was above buy a hold QQQ ETF return in the same period at around 46%, i.e., the random portfolio outperformed the index total return.

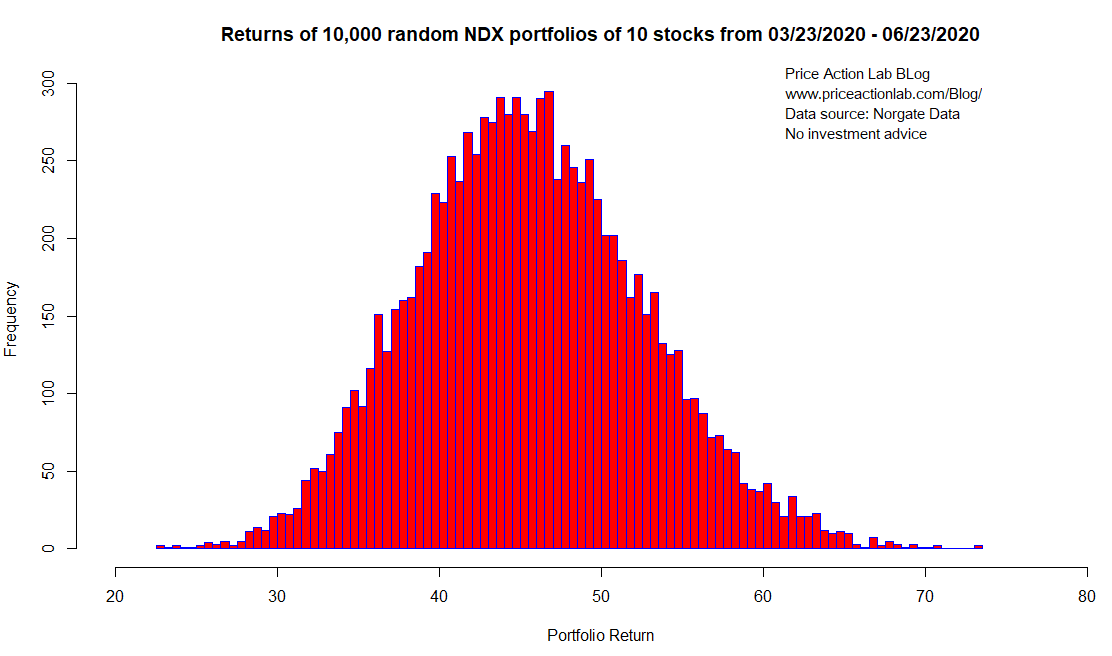

Next, we consider 10,000 random traders as above and we are going to generate the frequency distribution of the random portfolio returns.

The above distribution appears close to normal but the Lilliefors (Kolmogorov-Smirnov) test rejects normality and probably this is due to the right fat tail: there are some random traders that realized returns above 70%. The maximum return was 73.3% and the minimum return was 22.6%. The mean return was 45.5% and median return was 45.3%.

Therefore, in the ensemble domain, there is no QQQ outperformance: the mean return is 45.5% versus 46.2% for QQQ buy and hold. This was expected as the outperformance from lucky random traders was counterbalanced by the underperformance of the unlucky ones. However, there were no losers.

Next, let us see how these traders have done since 2010 after choosing at random 10 stocks at the beginning of each year and rebalancing the portfolio annually.

We used Norgate data for the NASDAQ-100 index that also include current and past constituents to remove survivorship bias from the backtests. We highly recommend this data service (we do not have a referral arrangement with the company.)

Minimum return is 74% and maximum is 887%. About 15% of random traders made more than the buy and hold QQQ total return at 498.5%. The mean return is 378% and median return is 363%. As it turns out then, the ensemble of random traders did worse than buy and hold total return and transaction cost was a factor that contributed to the underperformance. However many traders outperformed buy and hold and there were no losers.

It boils down to this and financial media often misses the point: there is a possibility that timing strategies may lose money even when no random trader loses. Unless there is a significant edge, buying and holding is a better strategy. Furthermore, some lucky ones will even outperform the benchmark due to luck with random trading. Felix Grandluckmeister (fictional character), the legendary investor, has admitted that.

Charting and backtesting program: Amibroker

Data provider: Norgate Data

If you found this article interesting, you may follow this blog via push notifications, RSS or Email, or in Twitter

Price Action Lab Blog Premium Content