Some have argued in financial media that bonds have not been acting as a good stock market hedge this year. However, the data say otherwise. Those who look for perfect hedges will find them only in hindsight.

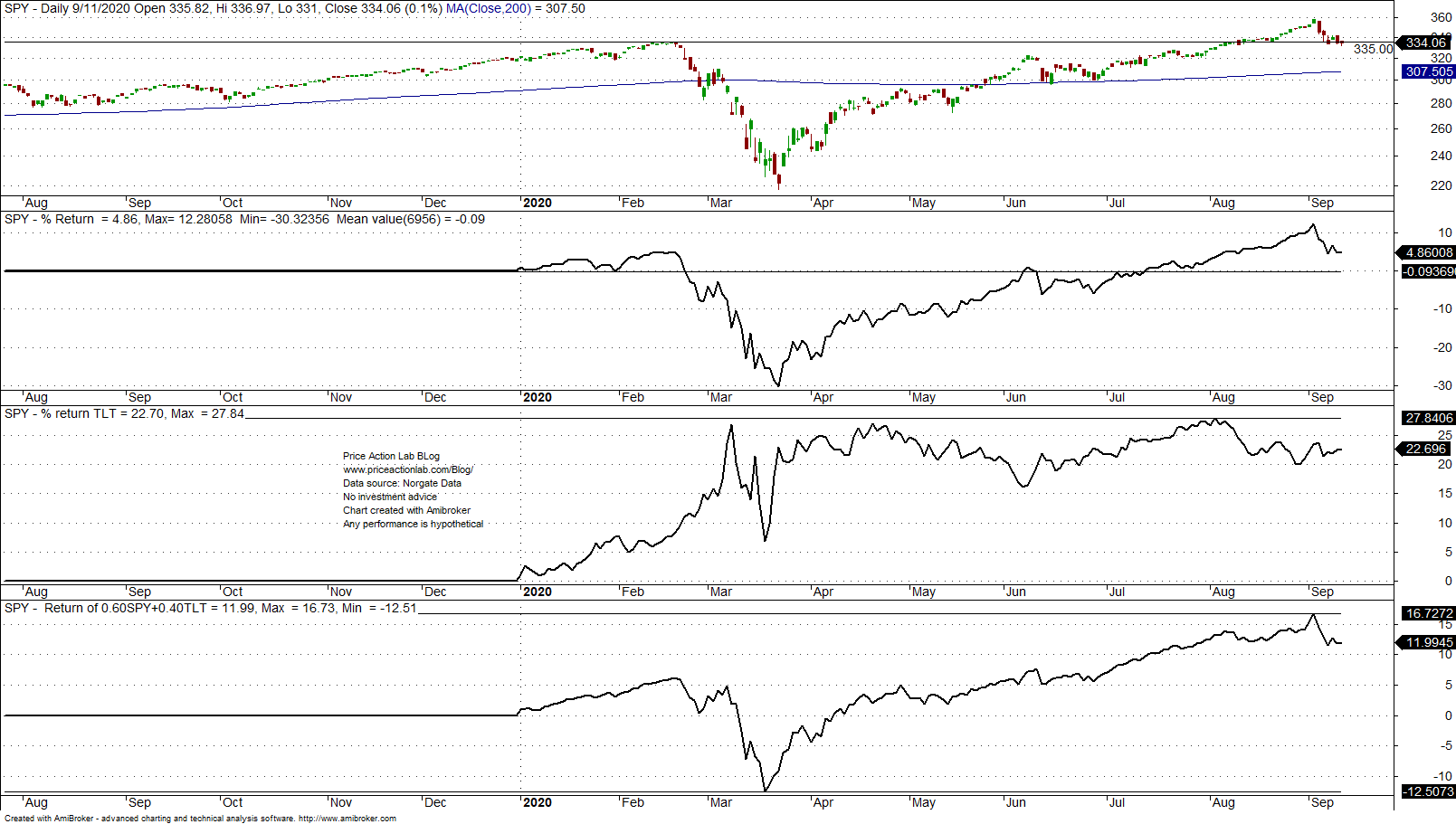

When SPY was down 30.3% earlier this year, the 60/40 SPY/TLT portfolio was losing about 12.5% for the year, as shown in the chart below.

Is this a bad hedge? Well, it depends on what would have been a good hedge. One can always find a good hedge in hindsight. The 60/40 portfolio is up about 12% year-to-date while SPY is up only 4.9%. This is because TLT is up 22.7% year-to-date after rising as much as 27.8%. How bad of a hedge is that?

It appears that many traders suffer from selective perception bias and focus only on down stock market days when TLT also falls. As the chart below shows, TLT has fallen on days that SPY has also fallen about 15% of the time since inception.

Needles to say the 60/40 portfolio is not free of tail risks. In 2007, the 60/40 portfolio suffered a 27% drawdown as was shown in this article. A 50% or larger drawdown is possible in case both stocks and bonds go on a downtrend. This can happen in the rare event of stagflation for example.

The perfect hedge exists only in hindsight. Although there are stories about stock market hedges with options and other derivatives, those can be accomplished successfully only in the context of an idiosyncratic alpha strategy and are outside the reach and capabilities of the average investor.

Charting and backtesting program: Amibroker

Data provider: Norgate Data

If you found this article interesting, you may follow this blog via push notifications, RSS or Email, or in Twitter

Price Action Lab Blog Premium Content