Although the US market has been mean-reverting for a while, buy on strength has also been a superior strategy. Below are analysis and some thoughts for further work.

The analysis below makes use of Norgate S&P 500 index and equity data. S&P 500 index data cover the period 05/20/1941 to 11/30/2020 and the equity data the period 01/03/2000 to 11/30/2020 and include current and past constituents to remove survivorship bias. We highly recommend this data service to those who would like to remove survivorship bias from backtests (we do not have a referral arrangement with the company.)

Buy on strength (BoS)

If the monthly return is greater than +5%, then buy at the close of the month and exit at the close of the month with return lower than -5%.

Mean-reversion (MR)

If the monthly return is lower than -5%, then buy at the close of the month and exit at the close of the month with return higher than +5%.

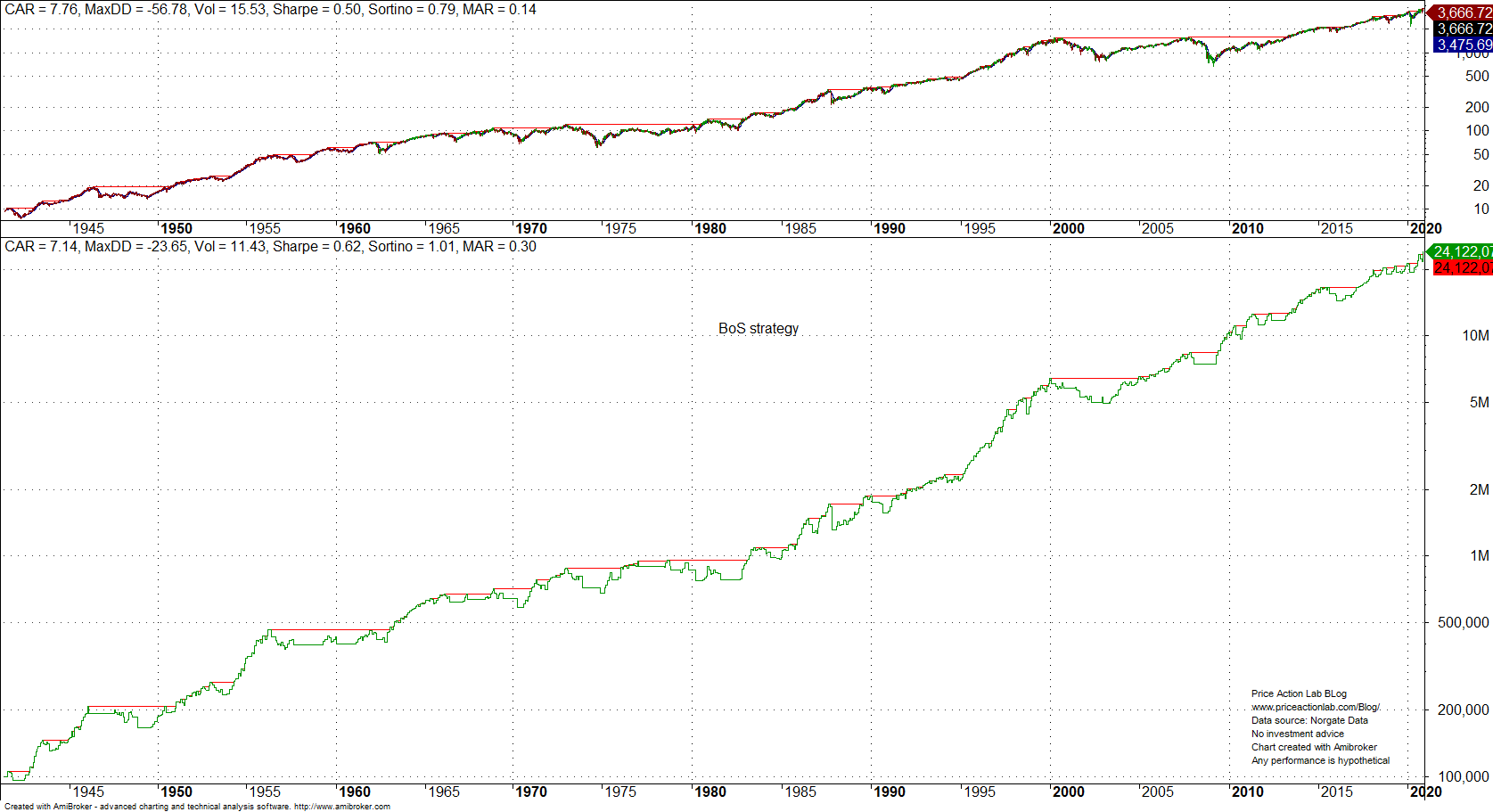

Case 1. S&P 500 index

Below are the results for the two strategies in the defined data period above.

| Parameter | BoS | MR | Buy and hold |

| CAGR | 7.1% | 0.5% | 7.8% |

| Max. DD | -23.6% | -59% | -56.8% |

| Sharpe | 0.63 | 0.1 | 0.50 |

| Trades | 47 | 46 | – |

| Average Trade | 15.5% | 1.6% | – |

| Win rate | 68.1% | 67.1% | – |

As expected, BoS is a superior strategy that outperforms buy and hold on a risk-adjusted basis with Sharpe of 0.63 versus 0.50. Below is the equity curve.

MR is a disaster with the strategy Sharpe barely positive. However, notice that the win rate of the two strategies is about the same at roughly 68%. The reason MR is a disaster is the low average trade in comparison to BoS. The latter strategy makes 15.5% on the average as opposed to only 1.6% for the former and that is a huge difference. Someone would expect that buying weakness should result in higher expected gain since the buy price is lower (buy low, sell high.) But no, this rule does not hold in general. In fact, buy high, sell higher is what has been working in the US market.

Case 1. S&P 500 index constituents

Next, we will test the two strategies with S&P 500 stocks with delistings included to remove survivorship bias. The strategies, BoS and MR, remain the same but we will be investing an equal amount of the equity in the top 10 stocks according to monthly returns ranking: for BoS we consider the 10 stocks with largest monthly return and for MR the stocks with largest monthly decline.

Below are the results for the two strategies in the defined data period for stocks.

| Parameter | BoS | MR | Buy and hold |

| CAGR | 10.6% | 7.7% | 4.4% |

| Max. DD | -49.4% | -79.5% | -56.7% |

| Sharpe | 0.5 | 0.22 | 0.22 |

| Trades | 662 | 881 | – |

| Average Trade | 4.1% | 2.9% | – |

| Win rate | 45.5% | 66.3% | – |

The Sharpe of BOs is double than that of buy and hold. MR Sharpe is equal to buy and hold but maximum drawdown is above uncle point and the strategy, despite matching buy and hold on risk-adjusted returns basis, it is again a disaster. Also note that win rate for MR remained high but for BoS decreased, as compared to Case 1. The main difference again between the two strategies is the larger average trade for BoS and this strategy outperforms buy and hold on both absolute and risk-adjusted basis.

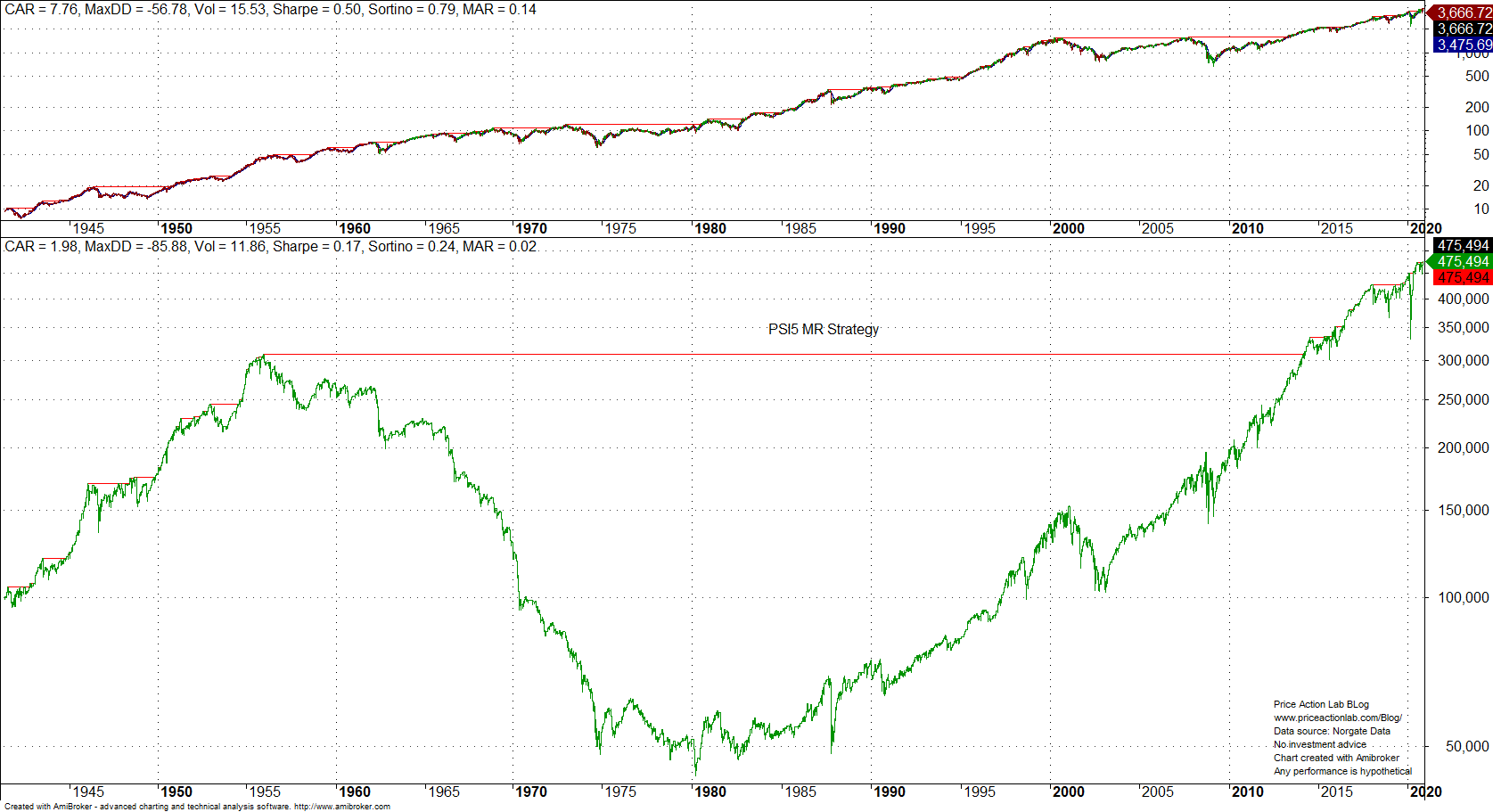

Why does BoS work but MR does not work well at all? Maybe if we look at the performance of our proprietary mean-reversion PSI5 strategy in S&P 500 index daily timeframe we may get an initial idea.

Mean-reversion undergoes regime changes. It worked well until 1955 but then reversed until 1980 (the reason for that has been discussed numerous times in this blog.) Then mean-reversion appeared again. It is possible that mean-reversion will have another regime change soon?

The regime changes could be the outcomes of predominant trading styles of market participants. If participants buy the dips, then mean-reversion has positive performance but if participants chase prices, then it has negative performance. Usually, when the market is dominated by algos, there is strong mean-reversion, but when it is dominated by unskilled human traders and investors that chase prices, then mean-reversion may undergo regime change. However, there is no clear demarcation in the markets and the system is too complex to decompose it into few regimes.

The conclusion from this brief analysis is that buy on strength is a more robust strategy that is less sensitive to regime changes as compared to mean-reversion, or buy on weakness, at least for now, caveat emptor.

Charting and backtesting program: Amibroker

Data provider: Norgate Data

If you found this article interesting, you may follow this blog via push notifications, RSS or Email, or in Twitter

Price Action Lab Blog Premium Content