Money on the sidelines, whether as a means of adding to a position after a large correction or raising cash during a correction, has not helped the performance of investors in US equities.

It sounds paradoxical, but it is true, and there is a reason behind the fact that money on the sidelines has not helped investors’ performance in US equities compared to buying and holding: the long equity market uptrends, especially in the 90s and 2010s. It’s highly likely articles have been written about this already.

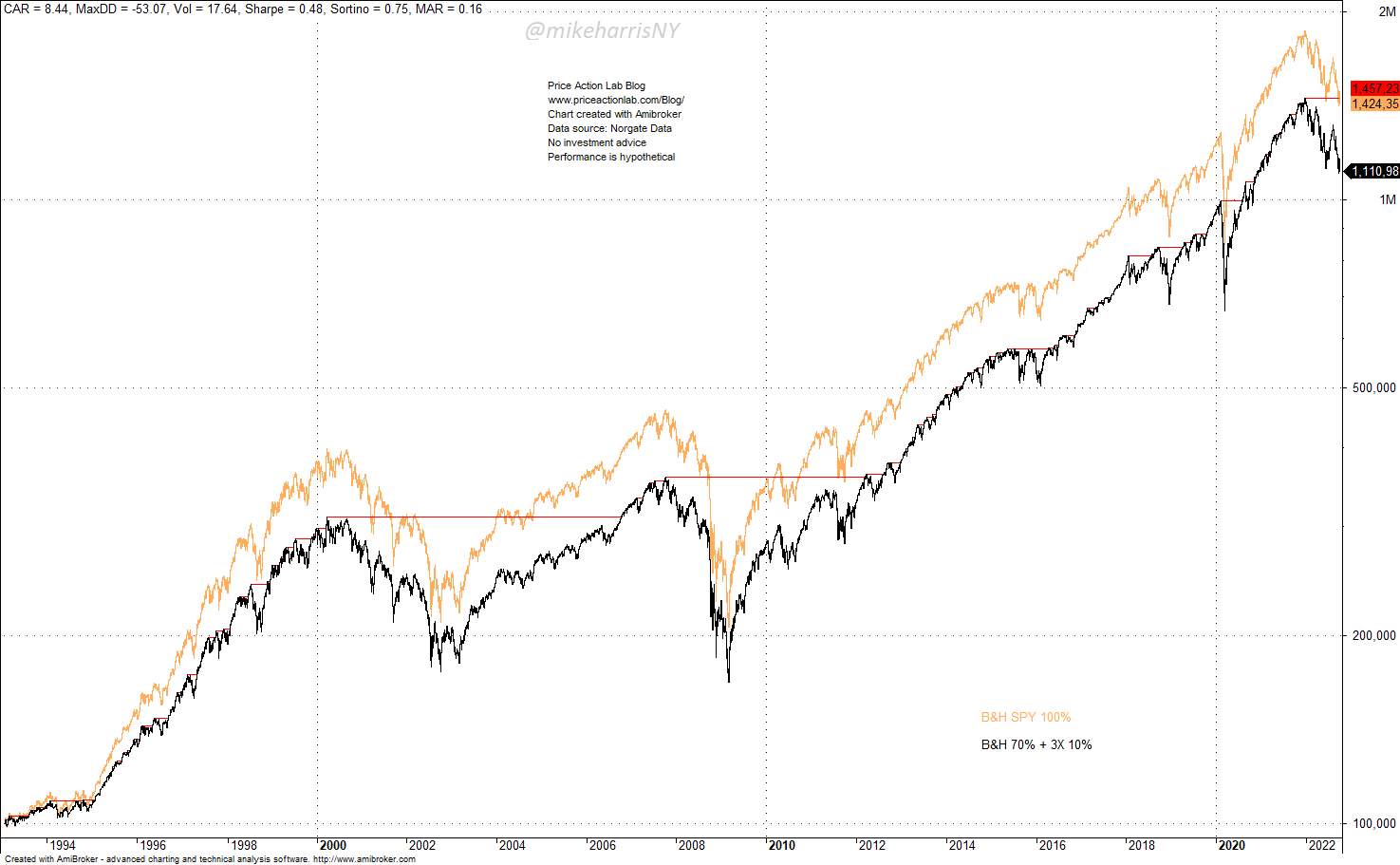

We’ll illustrate the adverse impact of money on the sidelines by considering an investor in SPY ETF’s inception (January 29, 1993) who decided to allocate only 70% and keep 30% to invest after the next market crash that wave theorists were expecting around 1995. After a drop of more than 30% from 252-day highs, the investor will add a third of the money left on the sidelines, and this can be repeated three times in the future.

The large correction many technical analysts were expecting by the mid-90s did not occur, and our hypothetical investor stayed underinvested during the 90s bull run but added 10% of the initial capital in 2001 when the market fell due to the dot-com crash.

Then, in 2008, 10% of the initial capital was added due to the GFC bear market. The final 10% was added during the 2020 pandemic crash. How did this investor do?

The performance of the investor was lower than buying and holding consistently, as shown below.

The black line is the equity of the investor and the orange line is the buy-and-hold equity. The maximum drawdown is about the same but the annualized return for the investor is 8.4% versus 9.4% buying and holding. Historically, waiting for corrections to add to positions was a waste of time and money.

The performance of strategies that vary exposure based on martingales (adding to position when equity drops versus an anti-martingale that reduces position) is path-dependent. There are possible paths where keeping money on the sidelines will result in better performance than buying and holding. However, these paths have not been part of the US market so far. As already mentioned, the two large uptrends, the irrational exuberance-driven of the 90s, and the quantitative easing-driven of the 2010s have insured investors with money on the sidelines were either punished or in the best case did not outperform buying and holding.

Below is an example with the same investment and mechanics as before, but with the starting date in January 2, 2000, just before the dot-com crash.

The investor (black line) outperforms buying and holding (black line) until 2007 due to lower initial allocation followed by a 10% addition based on the original equity in 2001. Then from 2009 to 2012, the investor again outperforms due to increasing position after a significant drop in equities of more than 30% during 2008. However, as the 2010s bull market evolves, the black line is absorbed by the orange line: the 10% remaining on the sidelines acts as a drag on investor performance, and the 2020 pandemic crash last addition is not enough to provide an edge.

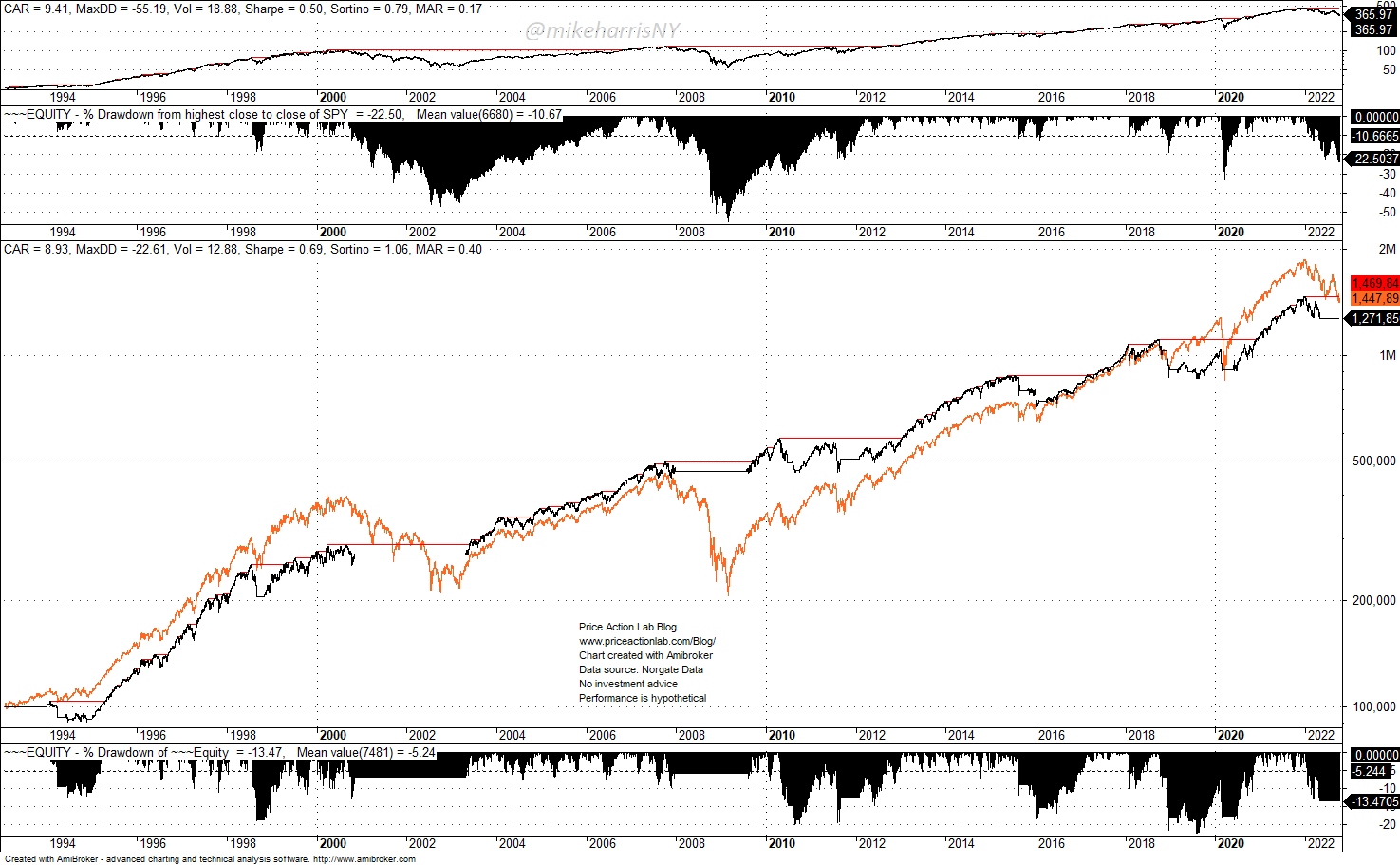

Below we look at the other definition of “money on the sidelines”: raising cash during corrections to invest later. The problem with this approach is that no one knows when a bottom is forming. Most investors end up chasing prices and add too late. As a result, these investors consistently underperform buying and holding.

We look below at the example of using the 12-month moving average to move in and out of the market at 100%. This is known as price series momentum.

The risk-adjusted performance of this method is superior, with a Sharpe of 0.69 versus 0.60 for buying and holding. However, absolute performance is lower: the annualized return of buying and holding is higher by about 50 basis points.

Note that even after the current correction, buying and holding (orange line) outperformance the price series momentum method (black line) in the history of SPY ETF. As mentioned before, performance is in general path-dependent and the starting point can have a large impact.

Conclusion

Due to specific conditions in the US stock market so far, including long uptrends and V-bottom recoveries from bear markets, “money on the sidelines” strategies have been punished and have underperformed buying and holding.

Conditions may change in the future and “money on the sidelines” could start offering a sound way of dealing with market risks. One of the major drawbacks of this approach to risk and money management for equity market investing is that predictions of when bottoms are formed are impossible. Therefore, “money on the sideline” often ends up chasing “invested money”.

For Limited-Time Only Premium Content Is 10% off for blog readers with the coupon NOW10

Disclaimer: The premium articles are provided for informational purposes only and do not constitute investment advice or actionable content. We do not warrant the accuracy, completeness, fitness, or timeliness for any particular purposes of the premium articles. Under no circumstances should the premium articles be treated as financial advice. The author of this website is not a registered financial adviser. The past performance of any trading system or methodology is not necessarily indicative of future results. . Read the full disclaimer here.

Charting and backtesting program: Amibroker. Data provider: Norgate Data