The image of the patient passive investor is probably wrong. These investors are the greediest and try to squeeze every basis point of return out of the market while blaming traders, the Fed, banks, and everyone else during bear markets.

Passive investing exploded after academics argued that tactical investing could not generate excess returns without taking an increased risk.

Before the emergence of the efficient market hypothesis (EMH) as the guiding investing principle, the market was dominated by value investors and stock pickers.

The EMH was the business plan of a multi-trillion dollar industry of “do nothing” fund managers. Since there is no way to beat the market without taking increased risks, most investors put their money in strategic portfolios, and the “do nothing” managers’ job is to receive contributions and keep the rebalancing right.

The EMH has been disputed by many market practitioners, some even famous, but remains the central theme of modern investing: low-cost passive investment vehicles are the key to success.

The EMH has driven greed to the extreme. The passive investor who believes they can squeeze every basis point of return out of the market is the greediest type due to not only aiming at maximizing performance but doing it at minimum effort.

Then, those challenging periods to the greedy thesis arrive in the form of bear markets and crashes: dot-com, GFC, pandemic, and now the inflation-driven correction.

What is the response of the greedy passive investor? Add more to the passive holdings and the Fed must pivot.

Passive investing is not only greedy but also cultivates tail risk for the whole economy. Surely, the millions of passive investors who expect profits but cannot rationalize where they will come from when they sell, have a significant impact on politics. The danger is the derailment of sound monetary and fiscal policy. The latter was seen in the UK in the last few weeks with severe ramifications.

It is not the market trader, or the active fund manager who is greedy. The greedy ones are the passive investors with the following objective function: to maximize profit and minimize effort. This objective function interferes with the inner workings of a healthy economy to generate high distortions and even tail risks.

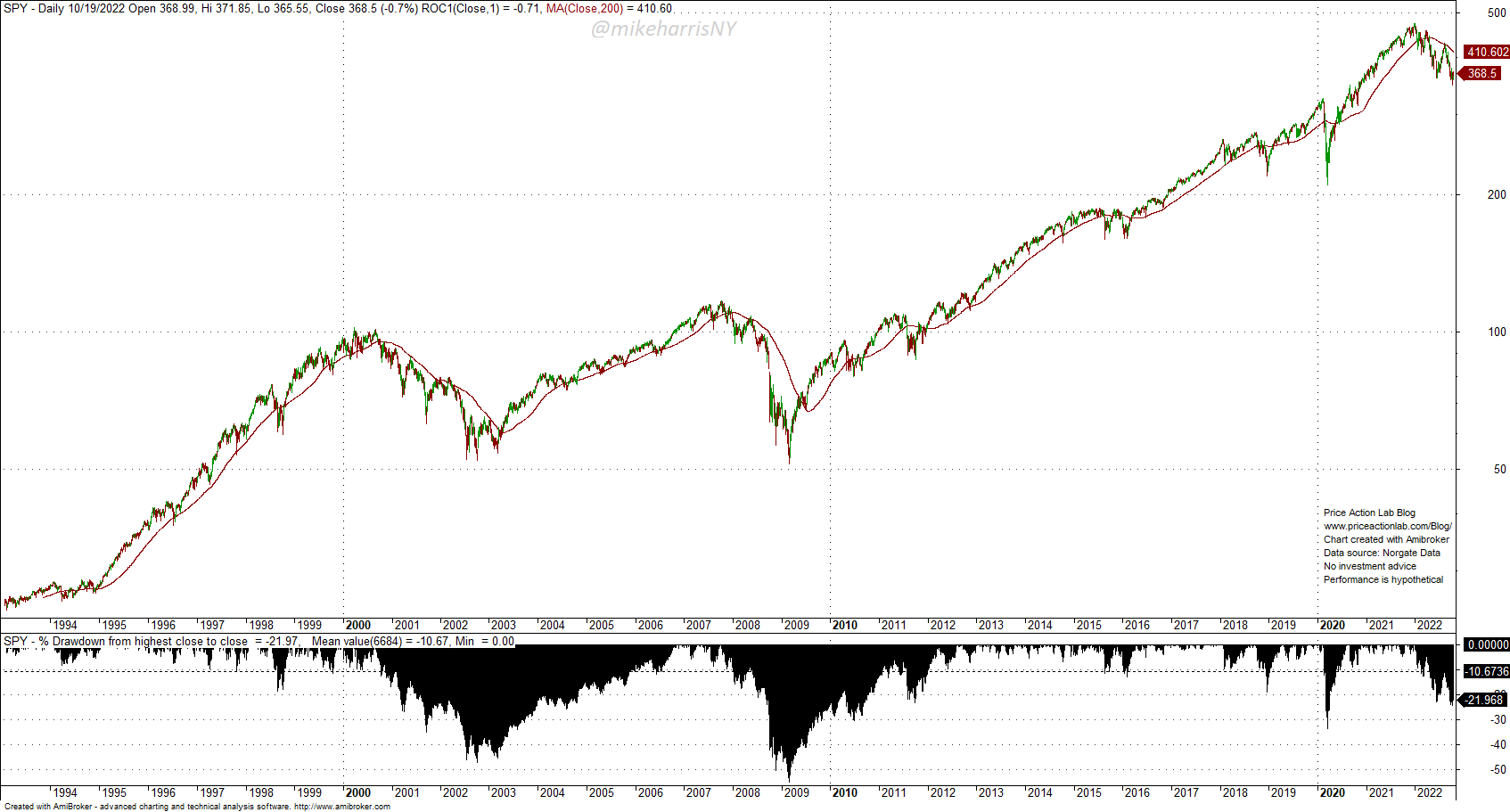

A 22% drawdown as of October 19, 2022, has caused an explosion in social media of messages that claim significant gains after large corrections. The intention is to appease the passive crowd and make sure they even add more to their passive portfolio. There is a problem, however.

The US equity markets have not experienced a long sideways chop period, as in emerging markets, for example, from 2011 to 2017. Although a multi-year consolidation is a low-probability scenario, at least one well-known fund manager thinks this will be the case for the next 10 years. If this scenario materializes, passive investing, and also momentum, will suffer the most.

It may be about time, because of the distortions in markets that passive investing has caused in the last 20 years at least. Markets should go back to their founding principle, which demands that investors assume risks to make returns. The Fed is not going to print forever to pay for the gains of passive investors. But they are doubling down, asking for a pivot amid one of the worst inflation periods in US history. Passive, greedy investing should not take the country down with it.

10% off all premium content, strategies, and software, with Discount Code NOW10. The discount is not valid with any other offers. The offer strictly applies to new purchases or extensions of existing subscriptions. Click here to subscribe.

Disclaimer: The premium articles are provided for informational purposes only and do not constitute investment advice or actionable content. We do not warrant the accuracy, completeness, fitness, or timeliness for any particular purposes of the premium articles. Under no circumstances should the premium articles be treated as financial advice. The author of this website is not a registered financial adviser. The past performance of any trading system or methodology is not necessarily indicative of future results. . Read the full disclaimer here.

Charting and backtesting program: Amibroker. Data provider: Norgate Data