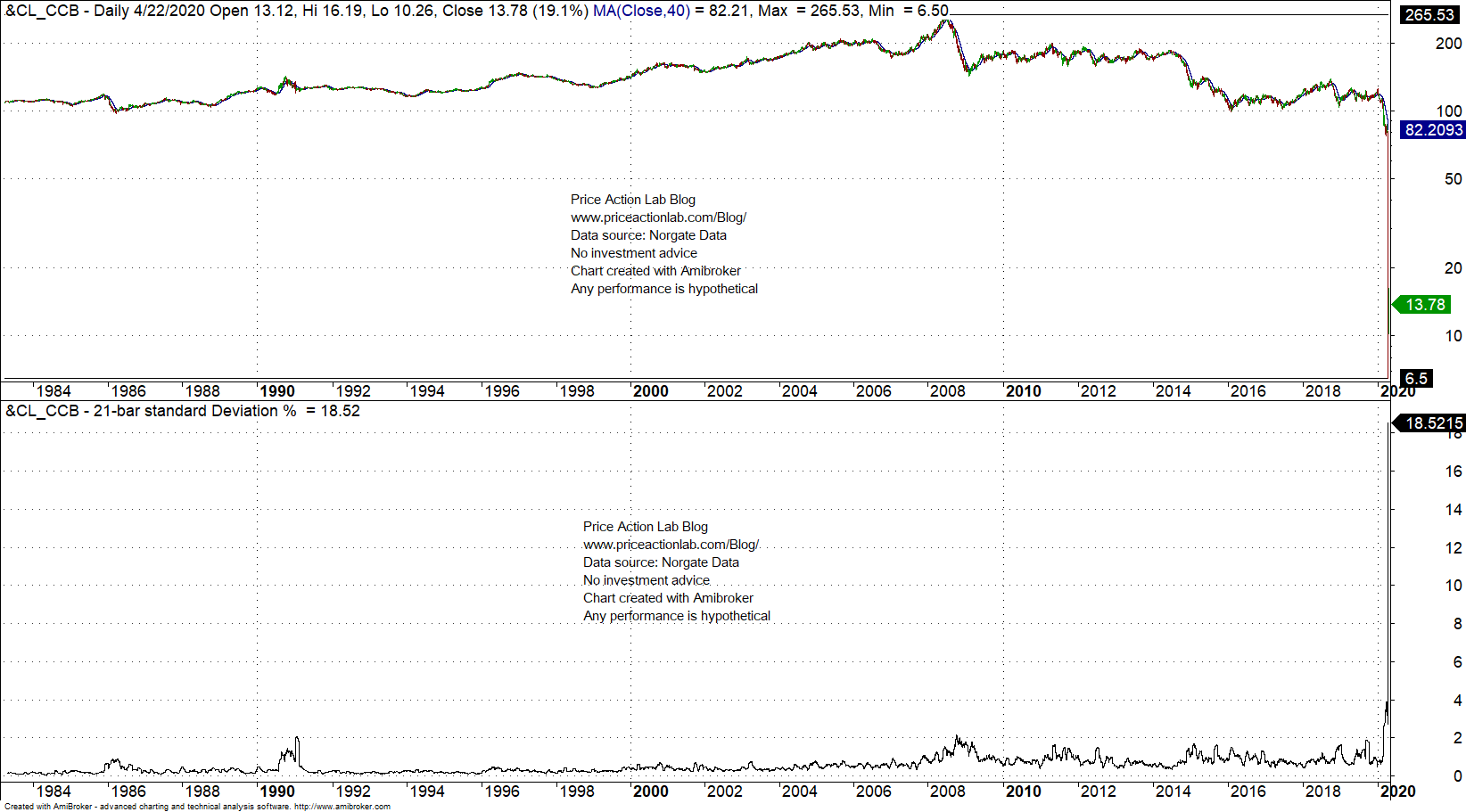

Backadjusted crude oil futures contracts absorb negative pricing but not the volatility spike.

Here is the daily backadjusted chart with 21-day standard deviation of daily returns. Data and backadjusting from Norgate.

Volatility surged to more than 18% from an average of about 0.5%

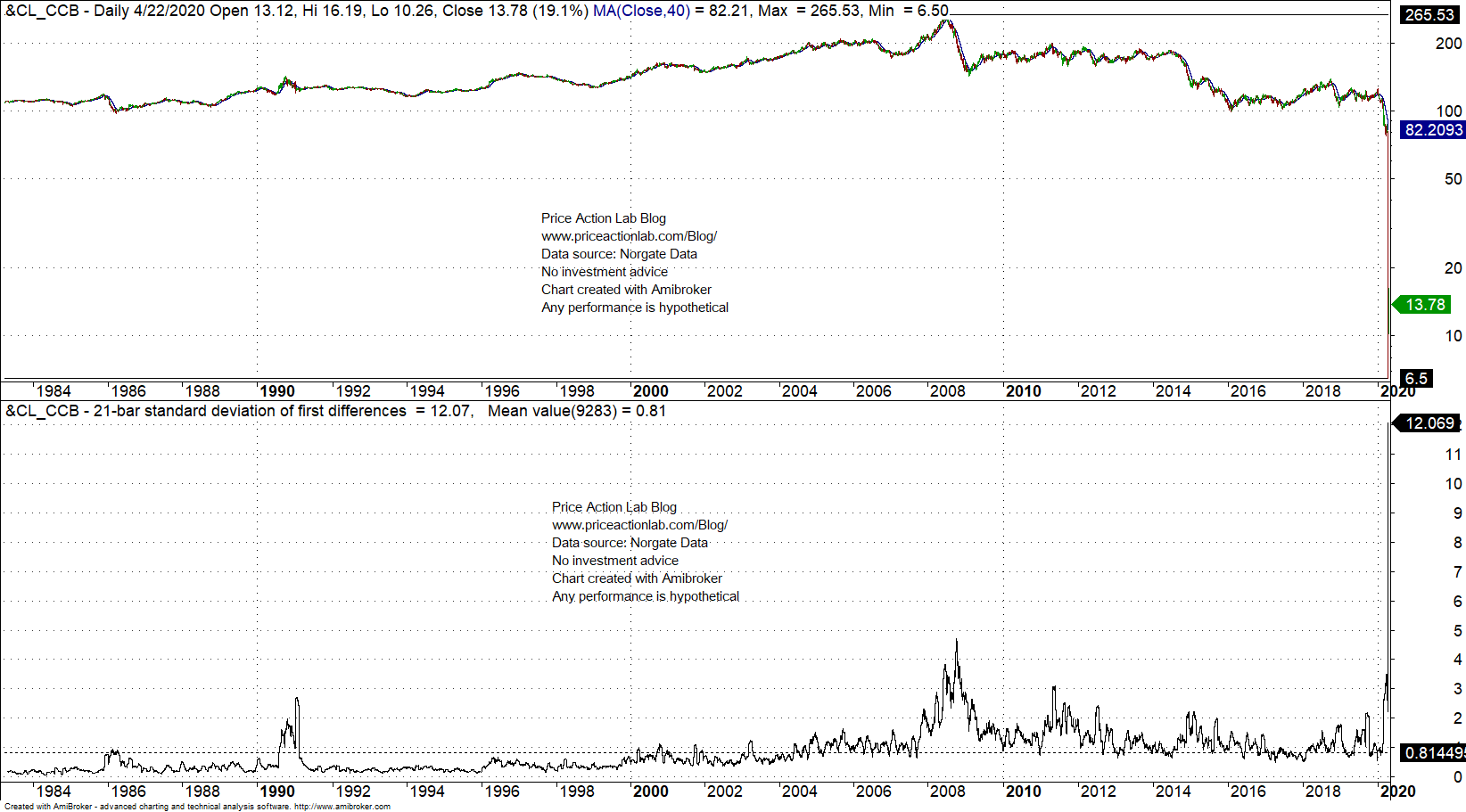

However, first differences (close-to-close change) are often more appropriate for futures due to “Panama method” of backadjusting.

The 21-day volatility of first differences surged from an average below one point to more than 12 points!

I find it interesting that this contract is still listed under these conditions. Maybe it should be delisted until market is back to “normal” and other type of contracts could be used for hedging and delivery. This behavior poses great risks to brokers but also to hedgers.

Price Action Lab Blog Premium Content

Charting and backtesting program: Amibroker

Data provider: Norgate Data

If you found this article interesting, you may follow this blog via RSS or Email, or in Twitter