DLPAL LS calculates four features for each security: P-long, P-short, P-delta, and S.

Definitions:

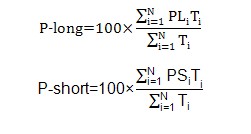

i= 1,…, N is the number of the features involved

PLi is the success rate of each strategy based on feature i for a long signal

PSi is the success rate of each strategy based on feature i for a short signal

Ti is the number of trades in the history of a security

P-delta = P-long – P-short

S is the significance of the result. S = 0 means the results are not significant.

Implementation in DLPAL LS

The program calculates the values of P-long and P-short for any combination of symbols and risk/reward parameters using a single workspace. A measure of significance S is calculated for each pair of values, P-long and P-short.

The user can specify the risk/reward parameters either as a percentage of the entry price or as a number of points added to the entry price of each trade generated by the strategies. Also, the exit at the close of the following bar is supported so that each trade is exited at the next close.

DLPAL LS also calculates ensemble features. These features are for a group of securities and include: avgPL, avgPS, Pratio, avgPLS, avgPSS

AvgPL is the average P-long value for the ensemble

AvgPS is the average P-short value for the ensemble

Pratio is the fraction of securities with P-delta (P-long-P-short) > 0

AvgPLS is the significance S weighted average P-long

AvgPSS is the significance S weighted average P-short

The results can be used to implement fixed models using the calculated features or as an input to machine learning algorithms.